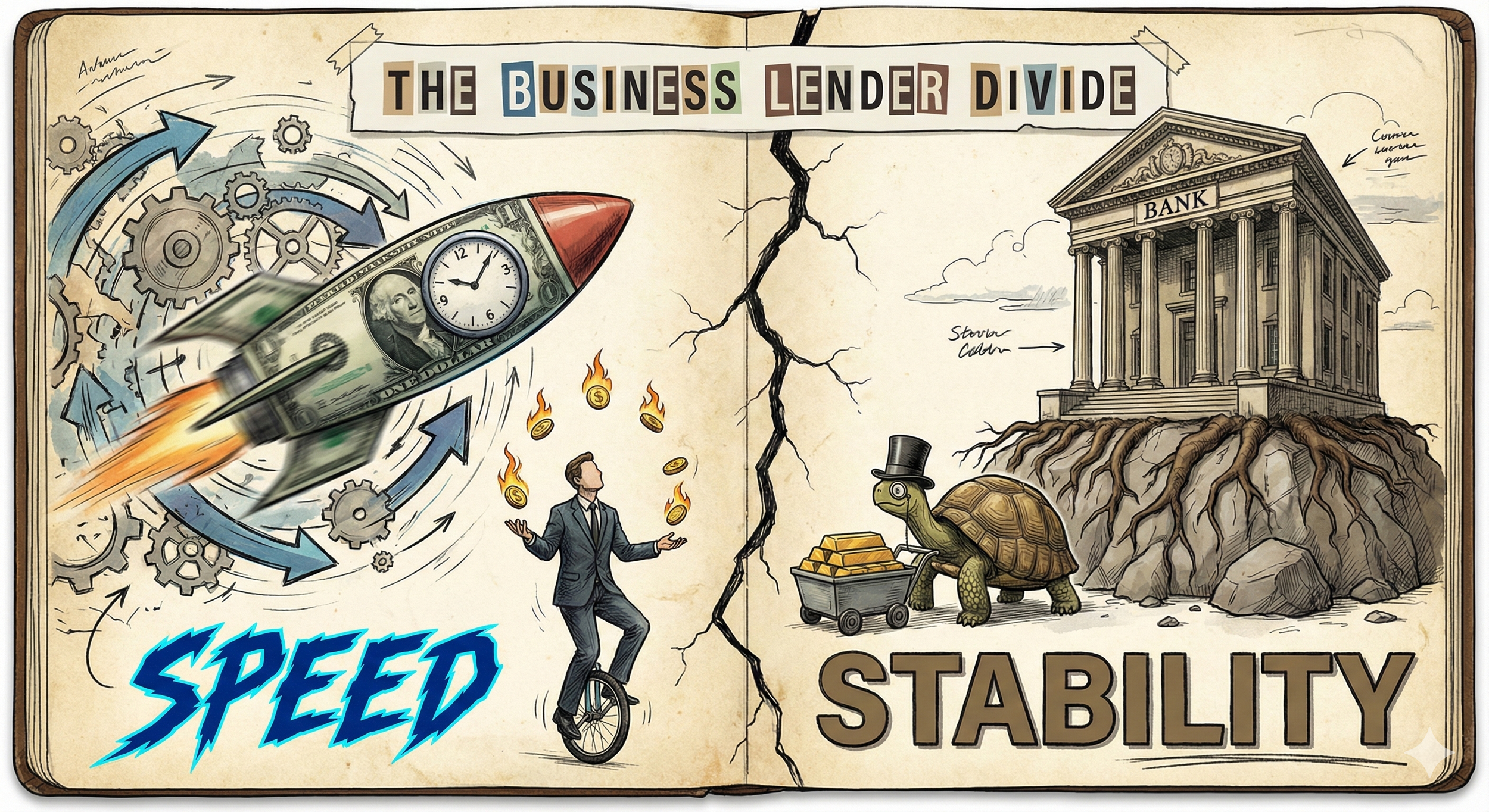

Every small business owner eventually faces the crossroads of capital. You need money to grow, to bridge a gap, or to seize an opportunity that just walked through the door. In that moment of need, the financial market presents you with two very different paths.

One path is paved with speed and accessibility but lined with aggressive demands that can choke your daily operations. The other path is steeper and harder to climb initially, but it leads to a plateau of stability and sustainable growth. This is not just a choice between two different loans; it is a choice between two fundamentally different philosophies of underwriting and two distinct futures for your business cash flow.

Understanding the difference between long-term, EBITDA-based underwriting and short-term, cash flow-only underwriting is the single most important financial lesson a founder can learn. It is the difference between renting money at an exorbitant daily rate and partnering with a creditor who views your success as their security.

To navigate this landscape, you must peel back the curtain on how these lenders think, how they measure risk, and why one model encourages aggressive timelines while the other fosters reinvestment.

The Reality of Short-Term Cash Flow Lending

The short-term lending market, often populated by Merchant Cash Advance providers and alternative fintech lenders, operates on a model of velocity. These creditors are not looking at your business as a long-term partner; they are looking at your bank account as a temporary resource.

Their underwriting process is deceptively simple and dangerously fast. They primarily scrutinize your recent bank statements, looking specifically at your daily average bank balance and your gross revenue deposits. They are less concerned with whether you made a profit last month and more concerned with whether enough cash cycled through your account to support a daily withdrawal.

This form of underwriting is often referred to as revenue-based financing. The "underwriter" in this scenario is often an algorithm designed to detect consistency in deposits. If you deposit ten thousand dollars a week, they calculate that they can safely siphon off a percentage of that flow without immediately bouncing a check. The risk assessment here is not about the long-term viability of your business model or your solvency over the next five years.

It is a bet on your liquidity over the next six to twelve months. Because the horizon is so short, the lender does not need to believe in your ten-year plan; they only need to believe you will stay afloat long enough for them to recoup their principal plus a hefty fee.

The Mechanics of Aggressive Repayment Timelines

The defining characteristic of short-term, cash flow-only underwriting is the repayment structure. Because these lenders perceive high risk and have no collateral security, they demand rapid repayment. This usually manifests as daily or weekly ACH withdrawals directly from your operating account. While a monthly payment allows a business owner to breathe, plan, and manage accruals, a daily or weekly payment is a relentless drumbeat that ignores the natural ebbs and flows of business cycles.

These aggressive timelines create a unique pressure on a business. When a lender requires repayment in six to eighteen months, the payment size relative to the loan amount is massive. A hundred thousand dollars borrowed over ten years might cost you a modest monthly sum, but that same amount borrowed over twelve months requires a debilitating daily outflow.

This structure forces the business owner to focus entirely on short-term liquidity. You stop managing for profit and start managing for the daily bank balance. Decisions become reactive rather than strategic. You might delay paying a vendor or skip a bulk inventory discount just to ensure the daily loan payment clears. This is the hidden cost of short-term underwriting: it steals your attention and forces you to operate in a state of perpetual emergency.

The High Cost of Convenience and Factor Rates

Short-term lenders rarely use an annual percentage rate to describe their costs because the number would be shocking. Instead, they use a "factor rate." They might offer you money at a one-point-three factor (1.3x), which sounds benign. It implies you pay back thirty cents on the dollar. However, when you calculate the cost of capital over a six-month term, the effective annual interest rate can skyrocket into triple digits. This expensive capital is a direct result of the underwriting method. Because they did not take the time to verify your assets, audit your financials, or understand your EBITDA, they must price in the risk of default.

This expense directly affects your bottom line, but more importantly, it affects your cash flow. Cash flow is the lifeblood of a small business. When you pay fifty cents of every dollar you earn to service expensive, short-term debt, you are starving your business of the fuel it needs to grow. You cannot hire new staff, upgrade equipment, or launch marketing campaigns because every available dollar is being funneled back to the aggressive creditor. The convenience of fast cash is paid for by the stagnation of your business growth.

The Cycle of Debt and Renewal Pressure

A particularly insidious aspect of short-term underwriting is the renewal cycle. Because the payments are so high and the terms so short, many businesses find themselves running out of cash before the loan is fully repaid. The lender, monitoring your balance, sees this stress and offers a solution: "renewing" the loan. They offer to give you more money, paying off the remaining balance of the first loan and depositing a small amount of fresh cash into your account. This resets the clock, often at the same or higher cost, and extends the term slightly.

This is known as "stacking" or churning, and it is a trap born from cash flow-only underwriting. The lender knows that as long as you have revenue coming in, they can keep the cycle going. They are not incentivized to help you become debt-free; they are incentivized to keep you perpetually servicing debt.

The underwriting criteria for a renewal are even looser than the original loan because they already have their hooks into your bank account. This cycle can continue for years, bleeding the business dry of its equity and preventing the owner from ever building true wealth.

The Stability of Long-Term EBITDA Underwriting

In stark contrast to the frenetic world of short-term lending stands the traditional, long-term credit market. This includes SBA lenders, private credit investors, and institutional non-bank lenders. Their underwriting philosophy is built on stability and projected performance over a long horizon. The gold standard metric for these lenders is EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. This acronym represents the operational cash flow of your business—the money your core business generates before accounting maneuvers and financial obligations come into play.

EBITDA-based underwriting is rigorous. It does not just look at your bank balance; it looks at your tax returns, your profit and loss statements, and your balance sheet. The underwriter is trying to answer a fundamental question: does this business generate enough true profit to service this debt over the next ten years while still having a buffer for errors? This process takes time. It requires documentation and patience. But the result is a loan structure that matches the lifespan of a business. It aligns the debt with the asset it is financing, ensuring that you are not paying for a long-term asset with short-term cash flow.

Understanding Add-Backs and True Cash Flow

One of the most powerful tools in long-term underwriting is the concept of "add-backs." A savvy underwriter knows that the net income on your tax return does not always reflect the true cash-generating power of your business. Small business owners legally minimize their taxable income through depreciation, amortization, and one-time expenses. EBITDA-based underwriting adds these non-cash expenses back into the equation.

Furthermore, they look for "discretionary" add-backs. These might include the owner's excess salary, personal expenses run through the business like a car or cell phone, or one-time legal fees that will not recur. By adding these back, the lender calculates an "Adjusted EBITDA," which shows the true amount of cash available to service debt. This is a far more accurate and favorable view of your business than simply looking at daily deposits. It gives you credit for the profit you are actually making, not just the revenue you are churning. This nuanced view allows long-term lenders to offer significantly larger loan amounts at much lower interest rates because they understand the real health of the organization.

The Strategic Power of Low Monthly Payments

The primary advantage of long-term underwriting is the amortization period. A standard SBA loan might have a term of ten years, and a commercial real estate loan might go up to twenty-five years. Spreading the principal repayment over a decade dramatically lowers the monthly obligation. This is the antithesis of the aggressive short-term model. Instead of a daily or weekly panic to cover a withdrawal, you have a manageable monthly expense that fits within your operating budget.

This difference in payment size is the key to business reinvestment. When your business debt service payment is low, the surplus cash flow stays in the business. You can use that money to hire a new salesperson who generates more revenue, or to repair a machine that improves efficiency. In the long-term model, business debt becomes a lever for growth rather than an anchor on operations. The lender becomes a silent partner who is paid slowly over time, allowing you to reap the immediate benefits of the capital. This alignment of interests—where the lender wants you to survive and thrive for the next decade—changes the dynamic of the relationship entirely.

Risk Assessment: Solvency vs. Liquidity

The inherent risks in these two underwriting models are viewed through different lenses. The short-term lender worries about liquidity risk: will you run out of cash on Tuesday? To mitigate this, they take their money first, every day or every week, often putting them in a "first lien" position on your cash flow. If you have a bad week, they still get paid, and you might bounce payroll. The risk is transferred entirely to the business owner and their employees.

The long-term lender worries about solvency risk: will your business model be viable in five years? To mitigate this, they require a Debt Service Coverage Ratio (DSCR) of usually one point two-five or higher (1.25x). This means for every dollar of debt payment, you must have one dollar and twenty cents of cash flow. This buffer is designed to protect both the lender and the borrower. It ensures that the business can absorb a downturn without defaulting. While the vetting process is stricter—often requiring collateral or personal guarantees—the structure is designed to prevent failure rather than exploit desperation.

The long-term lender is betting on your resilience, while the short-term lender is hedging against your collapse.

The Psychological Toll on the Business Owner

Beyond the math, there is a profound psychological difference between these two types of creditors. Dealing with short-term, aggressive creditors is stressful. Their collections departments are often ruthless, employing tactics like freezing accounts or filing UCC liens that can paralyze your ability to operate. This constant stress degrades the quality of leadership. A business owner worried about a daily or weekly debit is not thinking creatively about the future. They are operating in a "scarcity mindset," making fear-based decisions that often harm the long-term value of the company.

Conversely, long-term debt provides peace of mind. Knowing that your capital structure is stable and your payments are fixed for ten years allows an owner to adopt an "abundance mindset." You can plan for next year, negotiate better terms with suppliers, and build a culture of stability for your employees. The relationship with a bank or institutional lender is professional and advisory. If you hit a rough patch, a long-term lender is more likely to work with you on a deferment or modification because they are invested in the relationship, whereas a short-term algorithm simply triggers a default notice.

Choosing the Path of Sustainable Reinvestment

Ultimately, the choice between EBITDA-based and cash flow-only underwriting is a strategic decision about the trajectory of your company. Short-term debt acts like a shot of adrenaline: effective for a momentary burst but toxic if used as a daily or weekly sustenance. It serves a purpose for true emergencies or very short inventory turns, but it should never be the foundation of your capital structure.

Long-term debt acts like a strong foundation. It supports the weight of the business, allowing you to build upward. It preserves your cash flow, protects your margins, and respects the time it takes to generate a return on investment. As a business owner, your goal should always be to graduate from the chaotic world of short-term, revenue-based lending to the mature, stable world of EBITDA-based financing. By organizing your financials, maximizing your add-backs, and proving your profitability, you unlock access to the kind of capital that fuels not just survival, but true, enduring success.

What is the Best Way to Deal with Business Debt Payments that are causing Business Cash Flow issues?

It is NOT by stopping ACH payments.

It is NOT by taking on another business loan.

It is NOT ALWAYS a Refinancing

It is NOT by entering into a debt settlement program.

Find out the BEST strategies to get your Business back to where it was

More Business Finance and Strategy Articles: