The following is a case study from one of our recent business refinancing and restructuring engagements. The core issue is high-cost, short-payback financing (MCAs) are mis-aligned with the cash flow of the business, requiring payments in excess of what the business generates. You will see how financing like MCAs and other short-term and high-cost financing can quickly erode and destroy a company’s financial health.

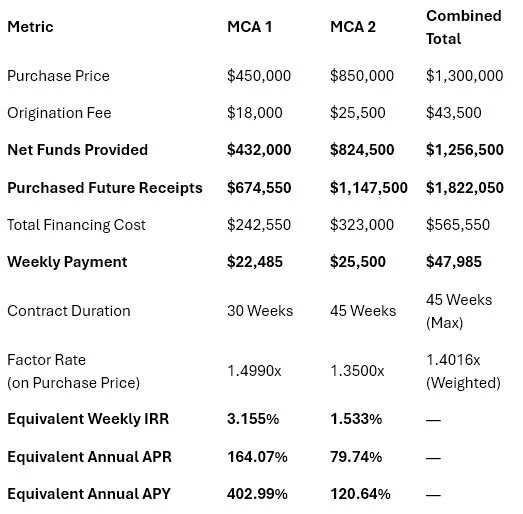

An analysis of the two Merchant Cash Advance (MCA) agreements reveals that their concurrent execution will place an immediate, unsustainable and highly destructive financial burden on the business.

The test-case business generates a healthy annual operating net income of $800,000 on approx. $15M of top line revenue (with a ~11.0% EBITDA margin), translating to a weekly debt service capacity of $15,385. However, the combined weekly debt service of two MCA financings during the first 30 weeks is $47,985 per week or more than three times (3.12x) what the business's operations can support in business debt service payments.

Because operations can only cover a small fraction of the weekly payments, the business is forced to use the very cash it just received / financed to pay back the lenders. Rather than injecting $1,256,500 in net growth capital, $1,129,742 of the funded principal must be immediately recycled and returned as business debt payments. This leaves only $126,758 of actual net usable capital, while saddling the business with $565,550 in high-cost financing fees and an effective annualized APR of up to 164%.

Detailed Contract Analysis & Proof of Accuracy

Below is the step-by-step financial breakdown of both contracts:

Immediate Detrimental Impacts on the Business

1. Severe Cash Flow Suffocation

Shattered Debt Capacity Limit: The business's sustainable weekly debt capacity is roughly $15,385 ($800,000 net operating income / 52 weeks). During weeks 1–30, the combined payment of $47,985 creates a weekly deficit of -$32,600. After Week 30 (when MCA 1 is repaid), the remaining payment of $25,500 still creates a weekly deficit of -$10,115.

The "Phantom" Capital Inflow: Over the 45-week period, the total cash repayment is $1,822,050, while the business's operations can generate at most $692,308 in debt service cash.

Recycling Principal: The business must pay the $1,129,742 shortfall directly from the $1,256,500 in principal it just received. Thus, 90% of the funded cash is immediately spent on paying back the funding companies, leaving a meager $126,758 of net cash for actual operations.

2. Immediate Destruction of Profitability

Wiping Out Net Income: The combined financing costs of $565,550 represent 70.69% of the business's entire annual net operating income ($800,000).

Profitability Reduction: If these fees are expensed during the 45-week contract term, the business's annualized net operating income will plummet from $800,000 down to a vulnerable $234,450.

3. Immediate Negative Equity & Asset Value Changes

Asset vs. Liability Mismatch (Negative Net Worth Impact): On day one, the business receives $1,256,500 in cash (asset increase) but incurs $1,822,050 in obligations (liability increase). This results in an immediate balance sheet equity write-down of -$565,550.

Destruction of Enterprise Valuation: Small businesses are commonly valued on a multiple of net earnings or EBITDA (e.g., 5.0x multiple). By reducing annualized net earnings by $565,550, these high-cost contracts would destroy up to $2,827,750 in the company’s enterprise value.

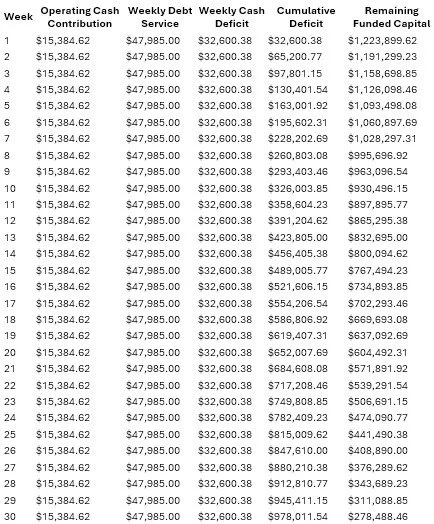

Here is the week-by-week deficit accumulation. This model assumes that the business receives $1,256,500 in total net funded cash at Week 0, generates a steady operating cash contribution of $15,385 per week (based on its $800,000 annual net profit), and applies all of it to meet the required payments.

Week-by-Week Deficit Accumulation & Capital Erosion

Key Observations from the Schedule

The Critical Drawdown Phase (Weeks 1–30):

During the first 30 weeks, the business loses $32,600 of its net cash liquidity every single week. By the time the MCA 1 contract is fully paid off at Week 30, the business has burned through $978,012 of its initial funds just to keep up with payments. Its cash reserve has shrunk to $278,489.

The Secondary Deficit Phase (Weeks 31–45):

Even after the MCA 1 contract is retired, the MCA 2 contract payment of $25,500 remains significantly higher than the business's operating capacity. The business continues to run a weekly deficit of -$10,115, draining the remaining cash balance down to $126,758 at Week 45.

The Trap Revealed:

Out of the $1,256,500 received, the business was forced to return $1,129,742 directly to the lenders. The business paid $565,550 in financing charges to essentially get a temporary $126,758 cash bump, leaving its operating treasury completely empty and vulnerable.

Restructuring Business Debt and Reigniting Growth

For many business owners, what begins as a necessary capital injection to bridge a gap or fund a promising new initiative can rapidly evolve into a suffocating cycle of high-interest, short-term debt. When daily or weekly payments begin to cannibalize operating revenue, businesses can quickly spiral from profitable enterprises into entities burdened by severe negative cash flow. This precarious financial state threatens not only the immediate survival of the company but also the long-term vision and livelihood of the founders and their employees.

Fortunately, a distressed balance sheet does not have to be a death blow for your business. Reversing this downward trajectory requires a strategic, multi-phased approach that prioritizes immediate cash flow stabilization followed by a comprehensive capital restructuring. The journey begins with transparent, mutual conversations with your current creditors to negotiate breathing room and halt the immediate cash bleed. Once the business achieves a break-even or slightly positive cash flow baseline, the focus shifts toward securing a permanent, sustainable financial architecture through private credit markets (a credit facility to draw on with a monthly payment pending underwriting).

By refinancing your obligations into manageable monthly payments over 24, 36 or even 60-months (ABL), you can slash financing costs by more than fifty percent and unlock the vital working capital needed to reignite your business growth.

The Trap of Short-Term and High-Cost Business Debt

Many small and medium-sized enterprises find themselves entangled in short-term financing solutions, such as Merchant Cash Advances or high-yield short-term loans, due to a sudden need for liquidity or an inability to secure traditional bank financing. While these instruments provide rapid access to capital, they are explicitly designed with aggressive payback structures. Instead of traditional monthly installments, these lenders often require daily or weekly automatic clearing house withdrawals directly from the business’s operating account.

Over time, this relentless withdrawal schedule creates a severe mismatch between when a business recognizes its revenue and when it is forced to service its business debt with payments. The high cost of capital associated with these advances means that a disproportionate amount of top-line revenue is diverted entirely to business debt service, leaving almost nothing for payroll, inventory, or basic operational expenses. Recognizing this trap is the crucial first step toward financial rehabilitation. Business owners must confront the reality that they cannot simply out-earn a predatory debt structure; structural intervention is an absolute necessity to prevent insolvency.

Recognizing the Need for Immediate Financial Intervention

Denial is a common and understandable psychological response when a business is facing overwhelming financial pressure. However, waiting until the bank account is entirely overdrawn severely limits your restructuring options. Business owners must proactively identify the warning signs of a critical business debt payments burden.

The most glaring indicator is a persistent negative cash flow directly attributable to business debt service, where the business is fundamentally profitable on a gross margin basis but operates at a net loss solely due to financing costs.

Another critical warning sign is the dangerous practice of taking on new short-term debt simply to pay off older short-term debt, often referred to as debt stacking. When you find yourself relying on expensive capital just to keep the lights on and service existing creditors, the business has reached a crisis point. Acknowledging this reality requires putting aside pride and looking objectively at cash flow statements. This honest assessment is the foundational prerequisite for initiating the conversations that will ultimately save the enterprise and begin the realignment process.

Initiating Mutual Conversations with Current Creditors

The prospect of contacting creditors to confess an inability to meet current payment obligations is daunting, but it is a critical lever in business debt restructuring. Contrary to popular belief, most creditors, even aggressive alternative lenders, prefer a modified, performing asset over a complete default and lengthy litigation process. Initiating these mutual conversations requires a blend of absolute transparency and a well-formulated plan of action. You must approach your lenders before you miss a payment, demonstrating that you are acting in good faith to resolve the situation. Best to work with a professional advisor here with experience in business finance and strategy planning.

When opening these dialogues, present a clear, unvarnished picture of your current cash flow realities. Show them exactly why the current payment structure is mathematically unsustainable. The immediate goal of these negotiations is not business debt forgiveness, but rather temporary relief to build up some cash liquidity. You are seeking a deferment or forbearance agreement, a temporary reduction in payment velocity or a shift from daily to weekly, or weekly to monthly payments. By securing these concessions, you artificially construct a liquidity runway, allowing the business to stabilize its cash position while you work on a permanent refinance solution through private credit markets.

Realigning Cash Flow from Negative to Break-Even

The immediate consequence of successful negotiations with your current creditors should be a rapid realignment of your business cash flow. By slowing down the aggressive drain on your operating accounts, the business is suddenly afforded a lifeline. This phase is not about achieving record profitability; it is entirely about stopping the financial bleeding and establishing a break-even baseline. Achieving this equilibrium is essential because it demonstrates to future, long-term investors that the underlying core business model is viable when it is not being choked by aggressive business debt repayments.

During this realignment phase, business owners must implement strict cash management protocols. Every dollar retained from the reduced debt service must be carefully allocated to sustain core operations, fulfill customer orders and maintain essential staff. This period requires immense discipline. The psychological relief of having more cash in the bank can sometimes lead to premature spending, but owners must remember that this is only a temporary patch. The true purpose of this break-even phase is to create the stable financial profile necessary to attract private credit investors for a comprehensive refinance.

The Pivot to Private Credit Investors

With the immediate crisis averted and business cash flow stabilized, the business must pivot aggressively toward finding a permanent capital solution. Traditional commercial banks are often bound by strict regulatory constraints and may view a recently distressed company as too high of a risk, regardless of the newly stabilized cash flow. This is where private credit investors and alternative institutional debt funds become invaluable partners for small and medium-sized businesses.

Private credit investors operate differently than traditional banking institutions. They possess the flexibility to look past temporary historical distress and focus instead on the fundamental viability, cash flow generation potential and intrinsic value of the business.

These lenders specialize in underwriting complex situations and are highly experienced in executing comprehensive business debt consolidation and refinancing transactions. By targeting private credit markets, business owners gain access to sophisticated capital partners who understand how to structure a facility that aligns with the specific operational realities and revenue cycles of the enterprise.

Structuring the Refinance Transaction

A successful business debt refinance transaction with a private credit investor is not merely a lateral move; it is a fundamental restructuring of the company’s balance sheet. The mechanics of this transaction involve the new lender providing a single, large credit facility that is immediately used to pay off all existing, high-cost, short-term creditors simultaneously. This effectively consolidates multiple fragmented and expensive liabilities into one cohesive financial instrument managed by a single institutional capital partner.

The most critical element of this new structure is the extension of the payback term. Instead of the suffocating 9-month to 12-month terms typical of merchant cash advances and other short-term business lending products, the new private credit facility will stretch the amortization schedule over 24, 36, or even 60-months for asset-backed lines of credit.

This structural elongation of the amortization (payback schedule) of the business debt is the primary mechanism that instantly transforms the company’s cash flow profile. By spreading the principal repayment over a timeline measured in years rather than weeks, the immediate burden on monthly revenue is drastically minimized, freeing up vast amounts of capital for the business to utilize internally.

Drastically Reducing Financing Costs and Eliminating Weekly Payments

The financial impact of transitioning from short-term alternative business debt to a structured private credit facility is immediate and profound. Short-term advances often carry annualized percentage rates that can easily exceed 60% or even 100%+ percent when factoring in origination fees and rapid payback schedules. By executing a strategic refinance, business owners can reliably target a reduction in their overall financing costs by more than 50% and even 70% to 90% reductions. These immense cash flow savings and interest cost savings drops directly to the bottom line.

Furthermore, this restructuring permanently eliminates the administrative and cash-flow nightmare of daily or weekly automatic withdrawals. The new credit facility will operate on a standardized, predictable monthly payment schedule. This shift from weekly to monthly installments allows business owners to accurately forecast their cash position, align their accounts payable with their accounts receivable, and operate their business with a sense of financial predictability that was previously impossible. The psychological and operational benefits of this change cannot be overstated.

Unlocking Working Capital for Future Operations

A properly structured private credit refinance transaction is designed to do more than just pay off old business debt; it is engineered to propel the business forward. When negotiating the new credit facility with private investors, business owners should not only seek the capital required to consolidate their liabilities but also an additional tranche of fresh working capital. This is a critical component of the recovery strategy, ensuring the business has the total liquidity (cash, cash-equivalents and credit) necessary to operate comfortably and take advantage of new opportunities.

Because the new debt is amortized over a much longer term at a significantly lower cost, the business can afford to take on this additional working capital while still maintaining a monthly payment that is drastically lower than their previous weekly obligations. This fresh capital acts as a vital cushion, protecting the business from unforeseen operational hiccups and providing the essential funding needed to restock inventory, launch delayed marketing campaigns or re-hire critical staff that may have been let go during the period of financial distress.

Reigniting Business Growth with a Stabilized Foundation

Armed with a consolidated balance sheet, drastically reduced financing costs, predictable monthly payments and an injection of fresh working capital, the business is officially positioned for a renaissance. The management team, previously consumed by the daily stress of simply surviving the next business debt withdrawal, can now refocus their energy and intellect on core business operations, customer acquisition, and strategic expansion.

The transition from a defensive, survival-oriented posture to an offensive, growth-oriented mindset is a monumental shift for the enterprise. The newly freed cash flow can be systematically reinvested into high-return areas of the business. Whether it involves upgrading technology infrastructure, expanding into new geographic territories or developing new product lines, the business finally has the financial foundation required to execute its vision. The narrative of the company changes from a story of distress to a compelling case study of strategic turnaround and renewed market competitiveness.

Building a Resilient Long-Term Financial Strategy

The ultimate goal of restructuring existing business debt is not just to survive a temporary crisis, but to build an unshakeable foundation for the future. Having successfully navigated the treacherous waters of negative cash flow and predatory lending, business owners must instill rigorous financial discipline to ensure history does not repeat itself. This involves establishing strict key performance indicators, maintaining a meticulous 13-week cash flow forecast and conducting regular audits of all capital expenditures and financing decisions.

Furthermore, the relationship established with the private credit investor should be nurtured as a long-term strategic partnership. As the business continues to grow and demonstrate consistent, profitable performance under the new capital structure, that same lender will likely be willing to provide additional, even cheaper capital for future expansion or acquisitions. By maintaining a clean balance sheet, honoring the new monthly commitments and prioritizing sustainable cash flow over rapid, unfunded growth, business owners can guarantee their enterprise remains resilient, profitable, and fundamentally secure for decades to come.