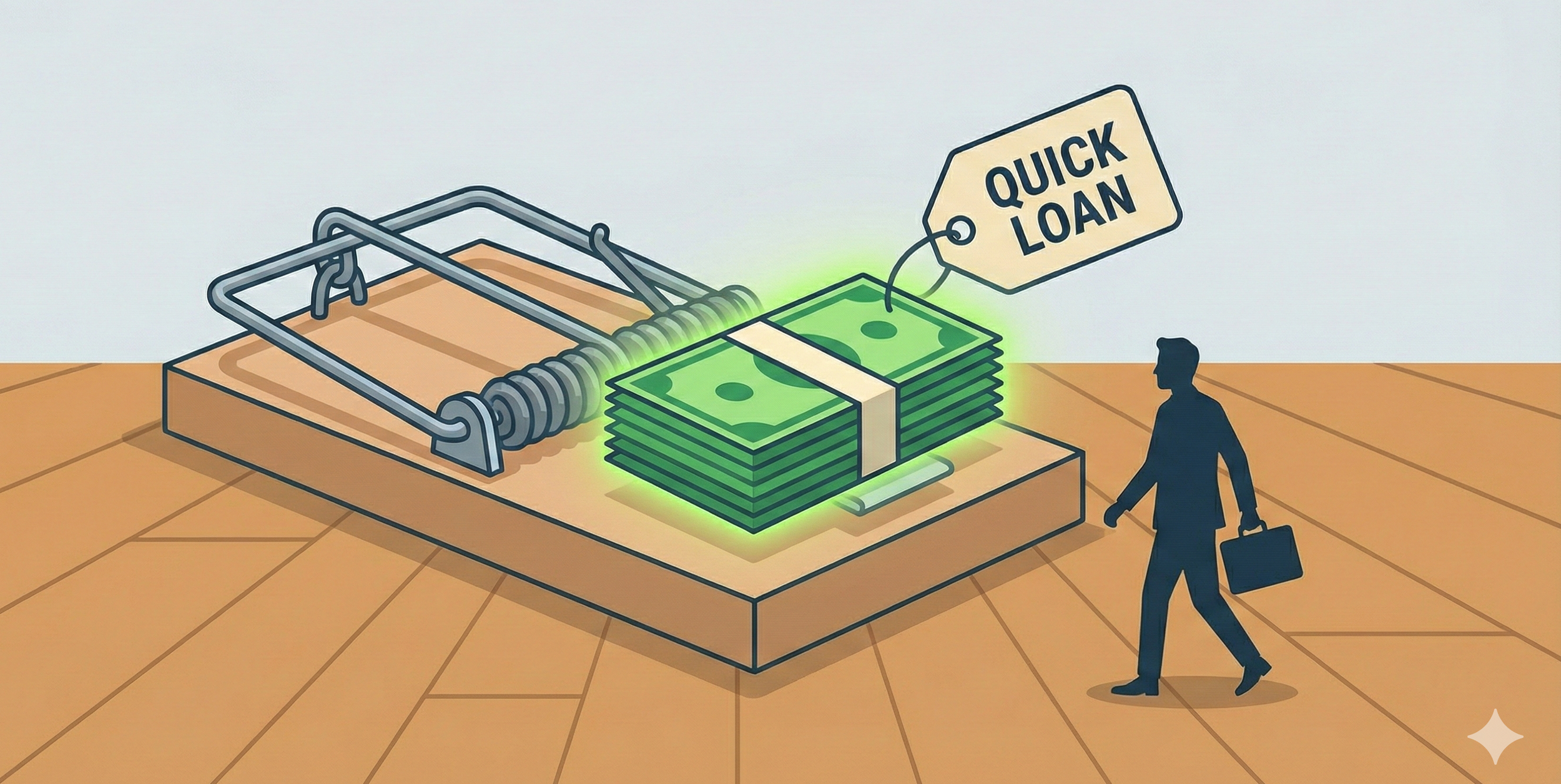

In the ecosystem of small and medium-sized business finance, there is a class of lenders or “funders” that functions less like a capital partner and more like an equity parasite. They don't care about your business plan, your legacy, or your employees. They care about one thing: the velocity at which they can siphon cash out of your operating account. While they brand themselves with sleek, modern logos and talk about "democratizing capital," they are, in reality, high-tech loan sharks.

The short-term lending space is built on a foundation of intellectual dishonesty. Underwriters in this sector are often nothing more than glorified data-entry clerks or automated scripts that ignore every principle of sound finance. They approve loans that they know a business cannot afford to make payments on without experiencing negative cash flow, and they bank on the fact that they can use aggressive, scorched-earth collection techniques to secure their profit before your company inevitably hits the wall. This is not lending; it is a controlled liquidation of your hard-earned equity. Pay or die.